Zimbabwe Takes a Stand

Lithium sits at the center of the emerging energy and industrial system, underpinning battery storage, electric vehicles, and a growing share of digital and defense infrastructure. Demand is rising quickly, but as with other critical materials, the challenge is not finding lithium in the ground. It is turning that resource into a stable, accessible supply that can support industrial scale.

The structure of the lithium supply chain has been relatively consistent. Countries extract raw material in places like Australia and Zimbabwe, then export and process it into battery-grade chemicals elsewhere. The result is a supply chain that appears geographically diverse but is, in practice, concentrated in a narrow part of the industrial base.

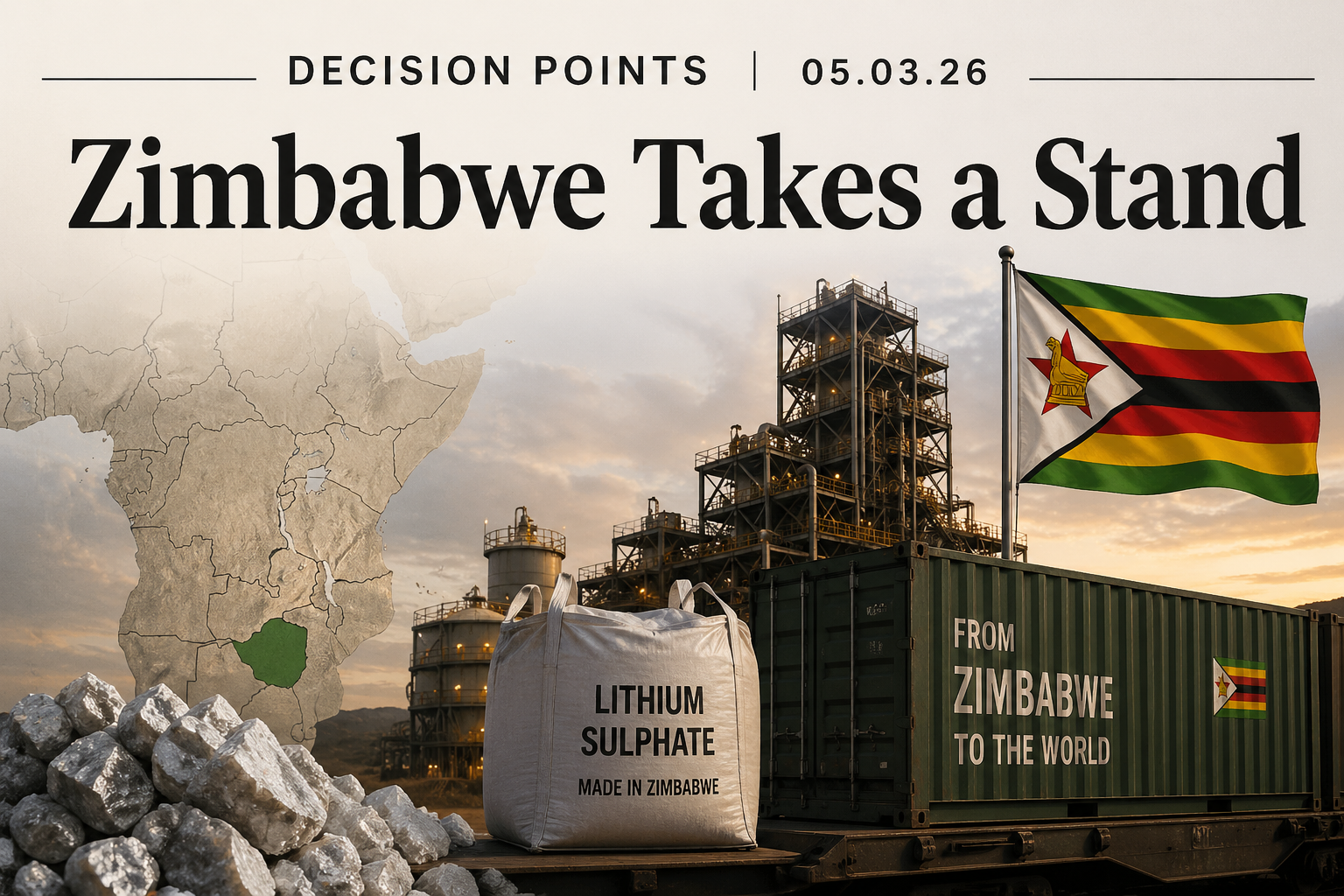

Earlier this week, Zhejiang Huayou Cobalt shipped the first consignment of lithium sulphate from its mine in Zimbabwe, marking the first time processed lithium has left the country instead of raw concentrate. The shipment came just two months after Zimbabwe halted exports of lithium concentrates, following concerns about how companies were exporting the material and allegations of corruption.

Zimbabwe has imposed a 10 percent tax on lithium concentrate exports while exempting processed material, and it has signaled that a full ban on concentrate exports will take effect in January 2027. Earlier this year, the government froze exports altogether, citing irregularities in how minerals were being shipped. These measures are already redirecting a flow that, until recently, moved almost entirely offshore. In 2025, Zimbabwe exported approximately 1.13 million metric tons of lithium-bearing concentrate to China, accounting for roughly 15 percent of China’s imports of that material.

The policy is straightforward. Zimbabwe is trying to retain a larger share of that value by moving into the next stage of the supply chain rather than exporting raw material and allowing it to be captured elsewhere.

Resource-producing states are starting to recognize that most of the economic return from critical minerals sits in processing rather than extraction. Moving up the value chain offers higher margins, more durable industrial activity, and greater leverage over how those materials are ultimately used.

Chinese firms are building processing capacity inside Zimbabwe instead of relying on facilities at home. Huayou completed a $400 million processing plant in late 2025 with the capacity to produce 50,000 metric tons of lithium sulphate annually, placing the conversion step between raw concentrate and battery-grade chemicals inside Zimbabwe rather than outside it. The location is shifting, but the structure is not. The output still feeds into the same downstream system, and the capability required to operate it remains tied to Chinese industry.

There is precedent for this model.

Indonesia implemented a similar policy with nickel, restricting exports of raw ore and compelling companies to invest in domestic processing. The result was a rapid buildout of smelting capacity within the country, much of it financed and constructed by Chinese firms. Indonesia captured more value from its resources, but the system that emerged remained closely linked to external industrial capability.

Other countries are exploring different approaches to the same problem. Chile has moved to increase state participation in its lithium sector, seeking to ensure that a greater share of the economic benefits remains under national control. While the mechanism differs, the objective is similar. Resource states are reassessing how critical minerals are developed and how the associated value is distributed.

The next stage of this shift may emerge in Zambia.

Zambia’s position is defined less by lithium than by copper and cobalt, both of which sit at the core of electrification and battery systems. Copper underpins power transmission, data infrastructure, and industrial equipment, while cobalt remains an important component in many battery chemistries. Unlike Zimbabwe, Zambia has not imposed broad restrictions on raw exports or mandated in-country processing at scale, but the same pressure is building.

If Zambia moves in that direction, the implications will extend beyond a single segment of the market. Lithium is closely tied to batteries, but copper and cobalt reach across a much wider portion of the industrial system. A shift in how those materials are processed and traded would affect infrastructure, manufacturing, and energy systems.

What is unfolding in Zimbabwe is part of a broader adjustment in how critical mineral supply chains are organized. Resource-rich countries are trying to move beyond extraction and into processing, using policy to reshape where value is created.

Whether that shift changes who actually controls the system remains unclear.